AeroTime is excited to welcome Michael Barnard as our columnist. Michael spends his time projecting scenarios for decarbonization 40-80 years into the future, and assisting executives, Boards and investors to pick wisely today. Whether it’s refueling aviation, grid storage, vehicle-to-grid, or hydrogen demand, his work is based on fundamentals of physics, economics and human nature, and informed by the decarbonization requirements and innovations of multiple domains. The views and opinions expressed in this column are solely those of the author and do not necessarily reflect the official policy or position of AeroTime.

For twenty years or more, electrifying everything has been at the top of climate change action plans. Mark Z. Jacobson’s 100% Renewables by 2050 modeling has spelled out the climate, air quality and economic advantages globally. Thought leaders including Saul Griffith, Hans-Josef Fell, Fatih Birol, and Mark Diesendorf from have been focused on this key solution as well.

It’s at the top of my Short List of Climate Actions That Will Work As Well. And it’s true across the transportation segment as well. All ground transportation — except for tiny niches like vintage cars — will be grid tied or battery electric. Bulk shipping will plummet with peak fossil fuel demand and batteries will power all inland and most short sea shipping, and biodiesel will power the rest.

But what about aviation? Those aluminum pressurized tubes hurtling through the air, 38,000 feet high, at a significant portion of the speed of sound, carrying hundreds of souls destined for work and play around the world?

Aviation is an outsized source of greenhouse gas emissions, but that’s not only due to burning kerosene. It also creates contrails, those evocative dual cloud strips in the sky, one of twenty of which are global warming disasters. And anything burned in our nitrogen-rich atmosphere creates laughing gas — nitrous oxide — which isn’t funny at all when we consider that it is 273 times more potent a greenhouse gas than carbon dioxide. A little goes a long way, and while ammonia fertilizer for agriculture is the worst nitrous oxide emissions offender, aviation contributes as well.

A common refrain from the aviation industry is that batteries aren’t fit for purpose for aviation. That’s inaccurate. They aren’t fit for all aviation purposes and will lead to business model and route changes, but they will be a much bigger part of aviation decarbonization than most analysts suppose.

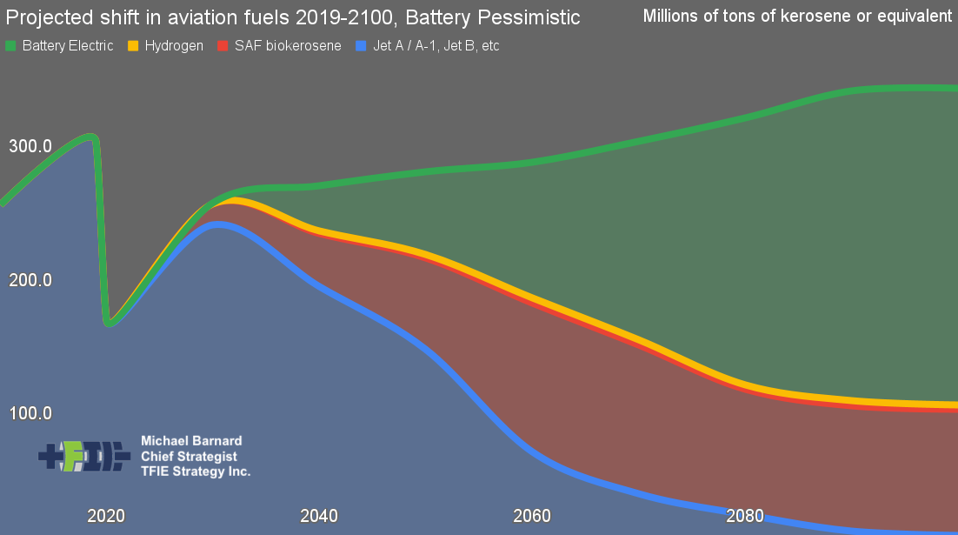

How do we read this graph? What does it tell us?

The first thing is that COVID-19 was a discontinuity in aviation growth and a fundamental transformer of the market. The 2019 to 2020 plunge in flights was real. It didn’t recover much in 2021 or 2022, not nearly as much as aviation marketers pretended. In a year or two, the post-COVID picture will be clearer and I’ll update this.

The second thing is that growth projections for aviation from the industry are not realistic. IATA and Boeing are projecting over 4% compounded annual growth for the next 20 years, and that’s not supported by anything other than pre-COVID curves projected linearly into the future. The extraordinarily rapid growth from the 1980s to 2019 was fueled by extraordinary changes in the global economy, but that period has come to an end.

The reasons for flatter demand are systemic transformations in our global economy. They include China’s transportation patterns, the end of China’s massive, double-digit growth, slower growth of non-China developing economies, peak population, remote work, increased costs of flights and more.

Is my projection of flatter growth accurate? No, of course not. The error bars are large. I will be off, likely by increasing amounts, with each decade. As with all my scenarios, all I assert is that they are less wrong than other projections.

Batteries, even in my battery-pessimistic scenario, will be sufficient for 70% of flights. Three-quarters of flights average 3,000 kilometers or less, and with silicon battery energy densities and hybrid SAF generators, 3,000 kilometers range with divert and reserve is achievable by 2040. Battery electric aviation will always have materially lower operation and maintenance costs, so any routes that can electrify, will electrify. This is an empirically proven truism, so repeat it to yourself regularly: anything that can electrify, will electrify.

I discussed earlier iterations of the aviation scenario with global experts on aviation demand, aerospace engineers and battery technologists. As I look back on my first version from three years ago, it hasn’t changed significantly. I have normalized the units to tons of kerosene to align with the maritime shipping scenario, and added the battery pessimistic scenario.

Peak fossil kerosene in 2030 will be below 2019 levels, or if not, so close to them as to be indistinguishable. The days of fossil fuel demand growth from aviation are over. There is room to remove fossil fuels from the mix more aggressively, something I’ll reserve as a consideration for future versions.

Sustainable aviation biofuels will dominate the next couple of decades of decarbonization. Biases against biofuels were fed by inadequate solutions and issues in the 2000s, but those biases will continue to fade. Modern biofuels will be made mostly but not always from waste biomass from our agriculture, food, lumber and livestock industries.

There’s more than enough waste biomass for long haul aviation and shipping requirements, which in my scenarios including this battery pessimistic scenario only add up to 180 million tons of diesel or kerosene annually. There are no land use or food concerns in an electrification heavy world, one where ground transportation, the vast majority of heating and electrical generation consume no fossil fuels.

There will be large pockets that are slower to accept this, for example the European Union, which is explicitly against crop-based biofuels but considers pelletizing forests for thermal electrical generation to be low-carbon. These will pass with time.

Battery electric aviation will eat the aviation market from the bottom. Regional air mobility will see fixed wing, conventional take off and landing pure electric and hybrid electric planes activating the thousands of smaller commercial airports that are underused. The useful parts of advanced air mobility — autonomous flight and digital air traffic control — will enable cargo and then passenger flights with even lower operational costs.

Origami electric rotorcraft like Joby and Archer will fail and much simpler electric rotorcraft scaling up from the drone market will continue to displace the helicopter market, taking more and more lifting burdens from crewed helicopters. That’s occurring today, with UAVs inspecting bridges, acting as aerial photography platforms, seeding and spraying fields, reforesting rugged terrain, carrying solar panels to hillside mounts and ferrying medical supplies to remote villages.

Volocopter, while at least avoiding the worst design excesses of the space, still failed to launch its one-passenger, zero-luggage curiosity ride at the Paris Olympics, something the rest will experience over and over again until investors’ money is gone. Simple passenger rotorcraft will be viable in the late 2030s, but none of the current entrants in the space will be around.

Each decade will surprise us again with battery advances. This year saw battery energy densities from CATL and others that serious analysts thought wouldn’t be on the market until 2050. It also saw battery prices below US$100 per kWh with CATL’s price list having lithium iron phosphate (LFP) batteries at $56 per kWh for fourth quarter delivery. Sub-$100 prices weren’t expected until 2030, and although LFP batteries aren’t suitable for aviation, that’s a clear signal that prices will continue to plummet as energy densities continue to climb.

In my battery-optimistic scenario transoceanic electric passenger flight will be viable starting in 2070. After that, a 30 year process of replacement of aircraft with engines with truly zero carbon equivalent, low noise battery electric drive trains would occur.

Sharp eyes studying the projection through 2100 will have noticed that hydrogen is a fraction of everything else, as well as the lack of synthetic Jet-A kerosene, with only biokerosene in the mix.

The hydrogen demand curve is simple. Biofuels need hydrogen as part of their processing for hydrotreating and hydrogenation. The amounts aren’t huge, with HEFA requiring 36 kilograms per ton of biofuel for example. Most of the hydrogen and carbon energy in the kerosene will come from the biomass we use to make them, provided by nature’s beneficence. Hydrogen is an industrial feedstock for biofuels, not an energy contributor. Aviation is already bunkering millions of tons of SAF biofuels, with Neste alone providing 1.5 million tons to Changi Airport in Singapore.

Hydrogen is a dead end as an aviation fuel. Gaseous hydrogen is far too low energy density by volume to provide any range. There is no path to certification for liquified hydrogen at 20° above absolute zero in the fuselage with human beings. There is no path to balancing center of gravity with liquified hydrogen inside a narrow body fuselage as it is consumed, so planes that flew any distance would nose down and fall out of the sky. The logistical complexity and cost of liquified hydrogen in aviation quantities in airports precludes its use.

As for synthetic fuels made from electrolyzed hydrogen and carbon captured from somewhere? Much more expensive than biofuels or batteries, so they just won’t be purchased, exactly as with maritime shipping, never mind fully electrified ground transportation. The International Energy Agency’s late 2023 update on e-fuels makes that clear, with costs for e-kerosene 5-6 times that of current Jet-A prices, and double biokerosene SAFs.

What about contrails? Flight path alterations driven by improved sensor sets and AI will negate the small percentage of contrails with the greatest global warming impacts.

This leaves nitrous oxides from jet biofuels as the remaining but much diminished concern. For the 70% of flights which will be battery electric even in the pessimistic scenario, emissions of nitrous oxides will not occur. The battery optimistic scenario would eliminate all contrails and nitrous oxide emissions.

Aviation will not grow nearly as quickly as it has in the past. Batteries and biofuels, in hybrid powertrain, fixed-wing aircraft will be quiet, low-carbon, low-maintenance and low-cost solutions to the remaining challenge. And the biokerosene all major manufacturers are certifying on today will bridge existing airframes and keep us crossing oceans.